Kaiji and the Trap of the Japanese Guarantor: Why One Stamp Can Swallow a Life

How Kaiji's guarantor scene draws on a real Japanese fear — the rentai hoshōnin system rooted in Edo-era goningumi collective responsibility and the weight of giri.

Tokyo-born, 3rd-generation Edokko · writing on Japanese culture from outside Japan

This article is also published on our Substack, where you can read and subscribe for free.

Read on Substack →

Kaiji and the Trap of the Japanese Guarantor: Why One Stamp Can Swallow a Life

Spoiler-Free Cultural Analysis

This article explores the real cultural and historical context behind a single setup detail in Kaiji — the moment a stranger arrives at the door asking about a debt. No major plot twists, no game outcomes, no character fates are revealed. Only the social mechanism beneath the scene.

Key Takeaways

- The Japanese 連帯保証人 (Rentai Hoshōnin: joint and several guarantor) is unusually severe by international standards because it makes the guarantor legally identical to the borrower, not a backup payer — and walking out of the borrower's life does nothing to release the guarantor.

- The cultural acceptance of this system has roots that reach back to the Edo-era 五人組 (Goningumi: five-household mutual responsibility group), where one person's failure was structurally borne by the surrounding network rather than absorbed by the individual.

- The dread Japanese viewers feel the instant the word 保証人 (Hoshōnin: guarantor) appears in an anime is not a fictional convention; it is a learned reflex shaped by 義理 (Giri: social obligation that is hard to refuse) on the asking side and absolute legal exposure on the signing side.

Key Terms Explained

- 連帯保証人 (Rentai Hoshōnin) / Joint and Several Guarantor — A guarantor who carries the same legal weight as the borrower from the moment of signing. The lender can pursue the guarantor first, without ever chasing the actual borrower.

- 保証人 (Hoshōnin) / Guarantor — The broader category. In ordinary Japanese conversation, the word usually carries the heavier 連帯 (Rentai: joint and several) implication even when not stated.

- 五人組 (Goningumi) / Five-Household Group — An Edo-period administrative unit where five neighboring households were collectively responsible for one another's taxes, conduct, and debts.

- 義理 (Giri) / Social Obligation — A moral debt to family, seniors, or close acquaintances that is socially very difficult to refuse, even when refusing would be the wiser choice.

- 判子 (Hanko) / Personal Seal — The carved name stamp used in place of a signature on Japanese contracts. The phrase ハンコを押す (hanko o osu: to press the seal) carries the same finality as "signing in blood" in a Western imagination.

The One Sentence My Family Repeated Like a Prayer

There was a sentence I heard so often growing up that I stopped registering it as advice and started registering it as weather. "Never agree to be someone's 保証人 (Hoshōnin: guarantor). Not for a friend. Not for family. Not for anyone." It came from my parents. It came from aunts and uncles. It came in the same flat, no-discussion tone that older Japanese relatives reserve for things they consider settled before you were born.

I never had to be told twice. The reason was a story that circulated quietly among the families I knew. A friend's father had agreed to be 連帯保証人 (Rentai Hoshōnin: joint and several guarantor) on a loan in the millions of yen. The borrower failed. The father — a salaried employee until that day — eventually ended up working part-time at a coffee shop. My friend ended up working night shifts at a factory. One stamp, one document, one small act of saying yes when saying no would have been socially awkward, and the entire family's career options had been quietly rewritten.

I have asked relatives to be my own guarantor twice in my life. Both said yes without much resistance, which I remember being grateful for and slightly unsettled by in the same breath. They had not absorbed the warning my own household had drilled into me. The very fact that the temperature gap between "people who would never sign" and "people who sign without flinching" is this wide inside one extended family is, I think, one of the quiet horrors of the system.

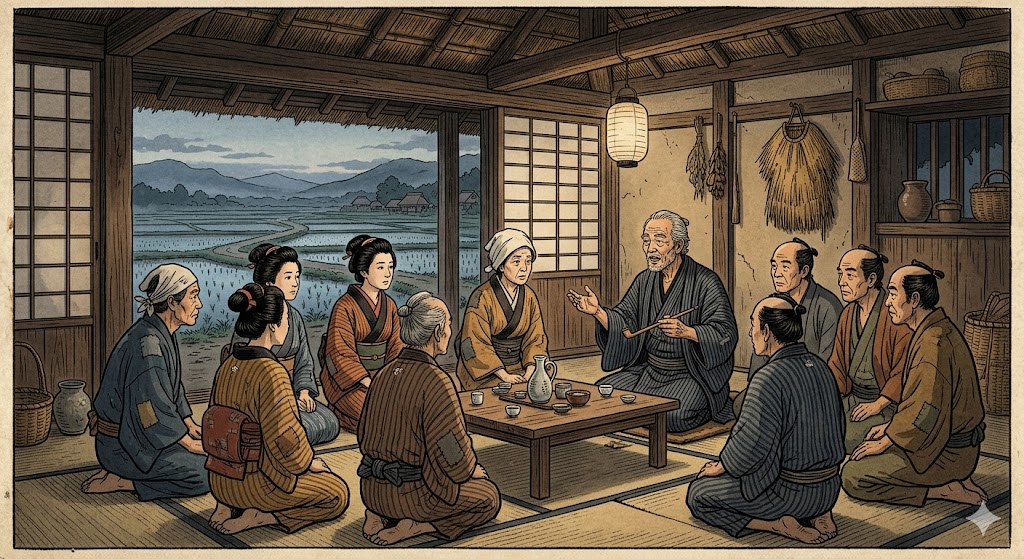

This is the layer Kaiji's first episode lands on. When Endō knocks on the door and produces the document Furuhata begged Kaiji to stamp a year earlier, the older Japanese audience is not watching fiction. We are watching the version of a story we already know, told with the lights turned all the way up.

A single press of the hanko on a guarantor document carries the weight of an entire family's future.

A single press of the hanko on a guarantor document carries the weight of an entire family's future.

Related: 進撃の巨人 (Shingeki no Kyojin) and the Walls of 村社会 (Mura Shakai): Why Japan Built Cages Long Before the Titans Came explains this in detail.

The Architecture of Catastrophe: Where the Hoshōnin System Comes From

To understand why a single 判子 (Hanko: personal seal) impression can erase a life in Japanese fiction, you have to understand that the system was never about backstopping a loan. It was about distributing responsibility across a human network.

The Edo Inheritance: Goningumi and Collective Liability

Under the Tokugawa shogunate, every village and urban block was organized into 五人組 (Goningumi: five-household mutual responsibility groups). If one household failed to pay its rice tax, the other four owed it. If one member committed a crime, the group was expected to know, report, and in some cases share the punishment. This was not a quirky local custom; it was a load-bearing pillar of how the state governed without a modern police force or credit bureau.

The point worth dwelling on is what this trains a society to assume. Trust does not live inside the individual. Trust lives inside the network of people surrounding the individual. The lender — whether a feudal authority or, centuries later, a consumer finance company — is not really evaluating you. It is evaluating who will be on the hook if you disappear.

The Modern Translation: Rentai Hoshōnin

When Japan modernized its civil code in the Meiji and post-war eras, the older instinct survived in a new legal form. The 連帯保証人 (Rentai Hoshōnin: joint and several guarantor) is not, in practice, a "co-signer" in the American sense. The lender does not have to first try to collect from the borrower. The lender does not have to prove the borrower has assets to seize. The moment the borrower vanishes — or even simply stops paying — the guarantor is the borrower for legal purposes.

In Kaiji's case, the 月20%の複利 (gettsu nijuppāsento no fukuri: 20 percent monthly compound interest) Endō produces from a chart is the dramatic flourish, but the real horror is structural. Furuhata pleaded with Kaiji to sign as guarantor, promising it would not cause any trouble. Kaiji stamped. Furuhata vanished. The debt did not vanish with him. It crossed the room and sat down on Kaiji.

Giri: The Pressure That Makes the Stamp Possible

The legal mechanism only works because of the social one. 義理 (Giri: hard-to-refuse social obligation) is the friction that prevents a sensible "no." A 先輩 (Senpai: senior at school or work) asks a 後輩 (Kōhai: junior). A relative asks a relative. A childhood friend asks. To refuse is not merely to deny a favor; it is, in the older social grammar, to declare publicly that you do not trust this person — a far heavier statement in Japan than in many other cultures.

This is why the warning "never sign as a 保証人 (Hoshōnin)" had to be drilled into Japanese children with the intensity of a religious commandment. The pressure to say yes in the moment is structurally enormous. The legal consequences of saying yes are structurally catastrophic. The only defense the older generations could pass on was a flat refusal taught early enough that 義理 (Giri) could not get a foothold.

The Edo-era goningumi system trained Japanese society to share one person's failure across the surrounding network.

The Edo-era goningumi system trained Japanese society to share one person's failure across the surrounding network.

What the Distance Lets You See

Living outside Japan for over a decade has changed what I notice about this. The first surprise was almost laughably small: when I signed my first rental contract abroad, no one asked for a guarantor. A few months of deposit, a passport copy, done. The contract was between me and the landlord, full stop. No relative, no employer, no childhood friend was being silently roped into my future.

This single absence taught me something I had taken for granted my whole life. The Japanese system, by demanding a 保証人 (Hoshōnin: guarantor) for things as ordinary as renting a small apartment, encodes a quiet assumption: the individual alone is not creditworthy enough. Reliability is something a network vouches for, not something a person carries on their own.

There is movement, though. Inside Japan today, individual rental guarantors are increasingly being replaced by 家賃保証会社 (Yachin Hoshō-gaisha: rent guarantee companies) — corporate intermediaries that, for a fee, take on the role a relative or senior would once have been pressured into. After the 2010s reforms to 出資法 (Shusshihō: the Capital Subscription Law) and 利息制限法 (Risoku Seigenhō: the Interest Rate Restriction Law) that eliminated the so-called グレーゾーン金利 (Gurē Zōn Kinri: gray-zone interest rates), the kind of monthly compound usury that Endō waves at Kaiji has lost much of its legal cover.

So the world Kaiji depicts — where a single signature, an absconding acquaintance, and a predatory rate of interest can detonate a life — is, mercifully, less common than it once was. But the deeper layer underneath is harder to dislodge. Walk through any Japanese workplace and you can still feel the 五人組 (Goningumi) inheritance: one person's mistake becomes the team's collective scolding, one member's scandal becomes the family's public shame, one resignation from the PTA reshuffles obligations onto everyone who stayed. The guarantor system was simply the most explicit, money-shaped version of a much wider social pattern.

When non-Japanese viewers ask me why the word 保証人 (Hoshōnin) hits Japanese audiences like a horror-movie sting, the honest answer is: because the legal system put a price tag on something the culture had been rehearsing for four hundred years.

Today, rent guarantee companies are quietly replacing the relatives and seniors who once carried that risk.

Today, rent guarantee companies are quietly replacing the relatives and seniors who once carried that risk.

FAQ

Q: Is 連帯保証人 (Rentai Hoshōnin) really treated the same as the original borrower under Japanese law?

A: Yes. The lender is not required to pursue the original borrower first or even to prove the borrower has been contacted. From signing day, the guarantor is legally indistinguishable from the borrower for collection purposes, which is the single most important fact non-Japanese audiences underestimate.

Q: Could Kaiji have legally refused to pay the inherited debt in real life?

A: Refusing the joint and several portion is structurally very difficult once the seal is on the document, but the specific 月20%複利 (monthly 20% compound interest) figure shown is an illegal usury rate even by the standards of the era depicted, and post-2010 reforms to interest-rate law have made such terms unenforceable in modern Japan.

Q: Is the guarantor system going away in Japan?

A: For ordinary consumer rentals, individual personal guarantors are being widely replaced by rent guarantee companies, and the most predatory lending practices have been curbed by legal reform. The cultural reflex of distributing responsibility across a network, however, persists in many other forms of Japanese social and professional life.

Key Insights to Remember

- The terror of the word 保証人 (Hoshōnin) in Japanese fiction is not a genre convention but a compressed memory of a real legal instrument. Kaiji's opening setup works on a Japanese audience the way a story about being uninsured in an emergency room works on an American one — the dread is borrowed from lived structural risk, not invented for drama.

- 連帯保証人 (Rentai Hoshōnin) is best understood as the modern descendant of 五人組 (Goningumi)-era collective responsibility, translated into the language of consumer finance. The throughline is consistent across centuries: trust is not a property of the individual but of the human network around them, and that network is the entity actually being underwritten.

- The slow shift toward corporate rent guarantee companies and tightened interest-rate law marks a quiet but important transition. Japan is gradually moving the burden of trust off the shoulders of individual relatives and seniors and onto institutional intermediaries — closing, piece by piece, the specific trapdoor that swallowed characters like Kaiji.

Sources

- Joint and several guarantor — Civil Code of Japan, Article 454 (English translation) — Japanese Law Translation, Ministry of Justice

- Goningumi — Edo-period collective responsibility system — Encyclopaedia Britannica

- Money Lending Business Act reforms and elimination of gray-zone interest — Financial Services Agency, Government of Japan

- Rent guarantee companies in the Japanese rental market — Japan Property Management Association

- Kaiji (Gyakkyō Burai Kaiji) — official series information — Nippon TV

About the author

Spoiler-free cultural deep-dives into anime, manga & live-action Japanese drama

- ●Tokyo-born, 3rd-generation Edokko (江戸っ子)

- ●Lifelong manga reader & anime viewer since the kaiju era

- ●Writes from outside Japan — distance as a cultural lens

- ●Spoiler-free · sourced · Kanji + Romaji + English

A Tokyo-born, 3rd-generation Edokko writer who has spent years living outside Japan. I use the anime, manga, and live-action Japanese drama you already love as a doorway into the folklore, language, religion, and everyday history behind them — written so even first-time fans can follow along, with sources for every claim.

Enjoy this article?

Get the next spoiler-free cultural deep-dive straight to your inbox.

Related Articles

Neon Genesis Evangelion and the Danchi: The Loneliness of Japan's Concrete Utopia

Why does Rei's crumbling apartment block say so much? A Tokyo-born writer traces the danchi — Japan's postwar housing utopia that families won by lottery — and how Evangelion spends its history to portray modern loneliness.

7/24/2026

Demon Slayer and Taishō Roman: Why the Demon Slayer Time Period Is the Only Era Where Demons Still Fit

How Demon Slayer uses the fifteen-year Taishō era and the aesthetic of 大正ロマン(Taishō Roman: Taishō Romanticism) to build a world where electric light and man-eating demons share the same night.

7/12/2026

The Apothecary Diaries and the Dokumiyaku: Inside Japan's Real History of Poison Tasting

How The Apothecary Diaries turns the poison taster into a quiet drama of power and risk, and what Japan's real 毒見役 system reveals about life near the throne.

6/29/2026

The Apothecary Diaries and the World of the Yūkaku: The Glamour and Cruelty Behind Maomao's Verdigris House

How The Apothecary Diaries opens a door onto Japan's yūkaku — the Edo pleasure quarters where the oiran's glamour and harsh debt bondage shared one address.

6/25/2026

Naruto and the Real Shinobi: What 忍 (Endurance) Meant Before Ninja Became Superhuman

How Naruto reframes the real shinobi and the kanji 忍 (endurance) — the patient, hidden intelligence work of Iga and Kōga spies behind today's superhuman ninja.

6/22/2026

The Apothecary Diaries and the Eunuchs Japan Refused: How the One Land That Copied China's Court Rejected Its Castrati

How The Apothecary Diaries dramatizes the eunuch-run rear palace, and why Japan alone refused China's castrati and solved it with the walled Ōoku.

6/15/2026